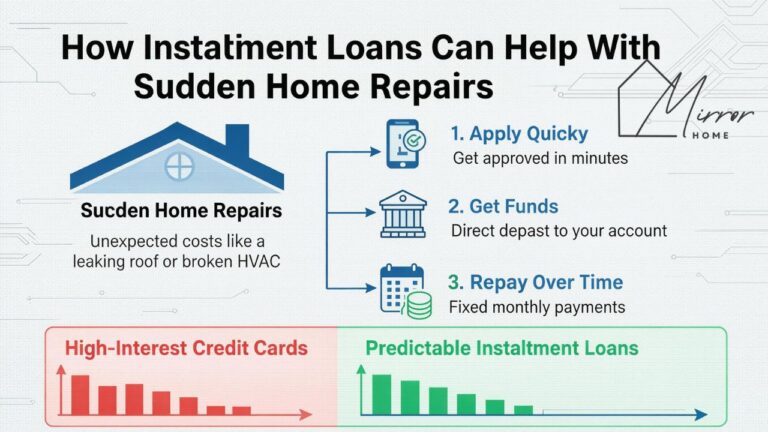

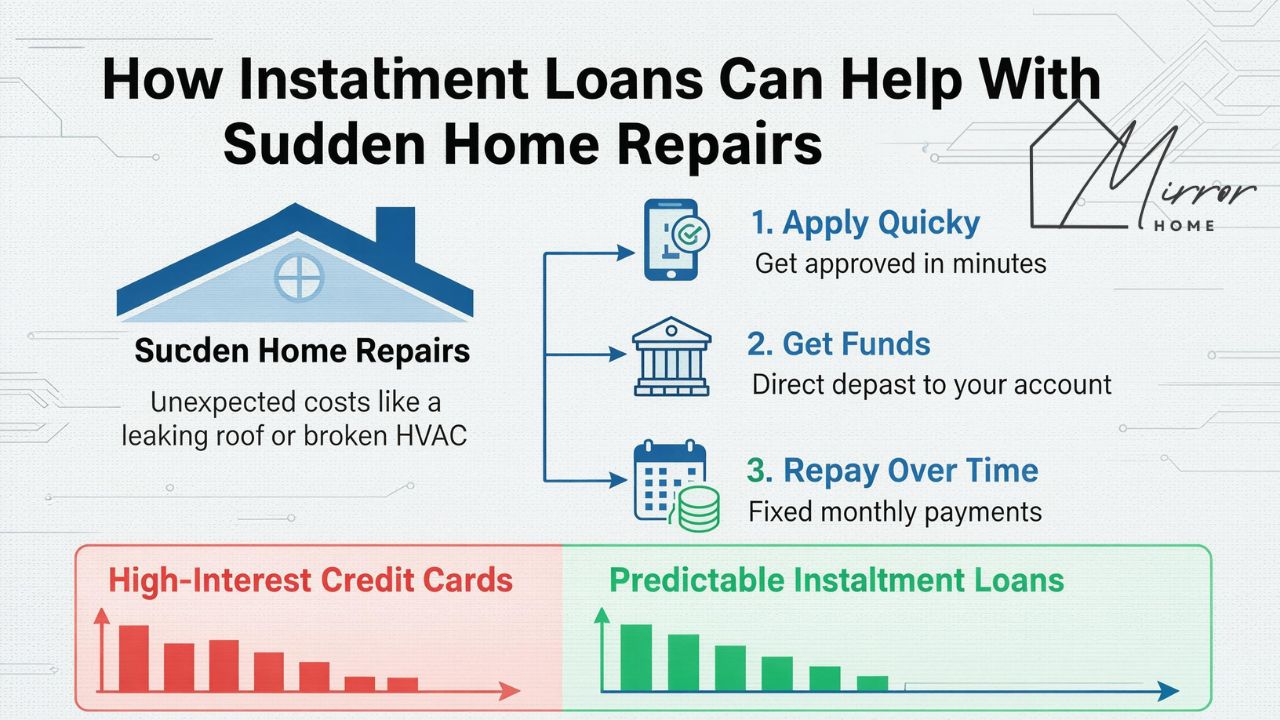

Sudden home repairs can disrupt even a well-planned household budget. A broken water heater, a plumbing issue, or a heating failure often requires quick action to keep a home comfortable and functional. When savings aren’t immediately available to address the issue, many households look for a structured way to cover the cost without delaying the work.

Installment loans can support that need by turning a large one-time expense into predictable monthly payments. This approach can help a household move forward with the repair, manage cash flow, and return to normal routines without the disruption and financial strain of a single large payment.

Home Repairs Demand Fast Funding

Many repairs are time-sensitive because they affect daily life. Hot water, working plumbing, dependable power, and comfortable indoor temperatures are basic needs that contribute to making any home livable. When a system fails, the household needs a solution that will allow for the payment of a contractor, purchasing parts, or replacing household essentials.

Even when a family budgets carefully, repair costs can throw off planning. Budgets still ned to cover the essentials such as utilities, childcare, groceries, and transportation. A sudden repair can pressure a budget that’s already stretched to breaking point.

Installment loans are often used to bridge the timing gap between income and unexpected expenditure. These loans provide a lump sum that can be used to pay a contractor or purchase materials, and spread repayment across a number of months. This structure can help maintain the household’s routine, especially when the budget simply cannot cope with the shock of a large, unplanned expense.

How Installment Loans Support Repair Costs

An installment loan provides a fixed cash amount upfront, which is then repaid through equal monthly payments over a set period. This model is useful for repairs because the cost is usually known after an inspection and a written estimate. The household can borrow a specific amount that matches the project and avoid overborrowing, which adds the risk of spending excess loan funds on non-essential items.

Approval and funding timelines vary by lender. Most lenders request proof of income, basic identification, and banking details for a deposit. Having these documents ready can speed up the process. The borrower can also prepare by calculating the required amount, the achievable target monthly payment, and the preferred repayment period.

Borrowers often compare online lenders, including loan places like world finance, when searching for installment loans with clear monthly payments. Reviewing multiple offers allows borrowers to understand how terms and pricing differ between lenders. Key details to focus on include the annual percentage rate, the total repayment amount, and any origination fees.

Creating a simple comparison spreadsheet can help organize these details and make the most suitable option easier to identify.

Estimating Costs and Picking a Practical Term

Accurate estimates help keep the loan aligned with the repair itself. A licensed contractor can provide a quote that outlines the full scope of work and expected expenses. This helps ensure the borrowed amount reflects the actual needs of the project.

A reliable estimate typically includes:

- Labor required for the repair or installation,

- Materials and replacement components,

- Permits or inspection fees when required,

- Any disposal or equipment removal costs.

As with any maintenance or repair, it’s always advisable to get multiple quotes from various reliable service providers. This will help pin down the exact loan amount required and avoid borrowing more than is absolutely necessary.

Loan term selection also affects how manageable the payments will be. A longer term generally results in lower monthly payments, while a shorter term often reduces the total amount repaid over time due to reduced interest payments. The most practical choice is one that fits comfortably within the household budget after essential expenses are covered.

Defining the purpose of the loan also helps keep spending focused. When the loan is tied to a specific repair, such as replacing a furnace or fixing a plumbing leak, repayment tends to remain more predictable and easier to manage.

Using Funds Efficiently During the Project

Once the repair is scheduled, households can use a simple system to keep spending organized. One approach is to keep all invoices and receipts in a single folder, either digital or paper, and record each payment with the date and amount. This improves clarity during the project and helps track the full cost.

Many contractors follow a milestone payment structure. The household can ask for a written quote outlining what each payment covers, such as materials ordering, installation or repair, and final testing. For appliance replacements, it can also confirm whether hauling away old equipment is included in the quote.

If the repair requires multiple purchases, prioritizing essentials helps. The loan should cover the core repair first, then any supporting items needed to complete it. If funds remain after the project is complete, applying the extra amount to the loan balance can shorten the payoff timeline and keep monthly cash flow manageable.

However, the borrower should ensure that the loan agreement allows for early payment without incurring additional charges or penalties.

Building a Clear Repayment Routine

A consistent repayment routine provides clarity and reduces stress. Autopay is useful for many households because it removes the need to remember due dates. For those who prefer manual payments, a calendar reminder and a dedicated payment date each month can provide the same structure and peace of mind.

Budgeting works best when the loan payment is treated as a fixed household expense. A simple method to ensure that the loan is manageable is to take income, subtract essential bills, and then confirm that the loan payment fits within the remaining amount, with room for additional expenses. If the payment feels unmanageable, selecting a different term or a smaller loan amount can create a better fit.

Some borrowers choose to make additional payments when extra income arrives. Even small extra amounts can reduce the remaining balance faster. A household can also build a repair reserve over time, even with modest (but consistent) contributions. This supports future maintenance planning and keeps the home livable.

Keeping the Home Running Smoothly

Installment loans can help households handle sudden home repairs by providing upfront funding and a structured repayment plan. With a clear estimate, a practical loan term, and organized use of funds, a household can complete essential work and keep monthly finances on track.

The most helpful approach is to borrow only what the repair requires, compare offers based on total repayment details, and maintain a consistent payment routine. This combination supports quick action to address emergency home needs while keeping the budget focused, predictable, and easier to manage.